.avif)

Not long ago, crypto and banks were seen as opposites. One promised freedom from centralized control, the other represented everything crypto wanted to escape.

But 2025 tells a different story. Once dismissed as a bubble by much of traditional finance, crypto is now being explored — and, in many cases, adopted — by some of the world’s largest banks. They’re running custody platforms, tokenizing bonds and gold, and piloting stablecoin initiatives. Regulators are shifting from blanket restrictions to structured rules that bring clarity and confidence.

At Mezen, we see this shift up close. We’ve helped banking clients explore stablecoin development and launch crypto-card programs, so we know how fast institutions are moving. That’s why we set out to do this research — to better understand the processes now unfolding at the intersection of traditional finance and crypto, and how these two worlds are blending into one financial system.

The numbers that prove it

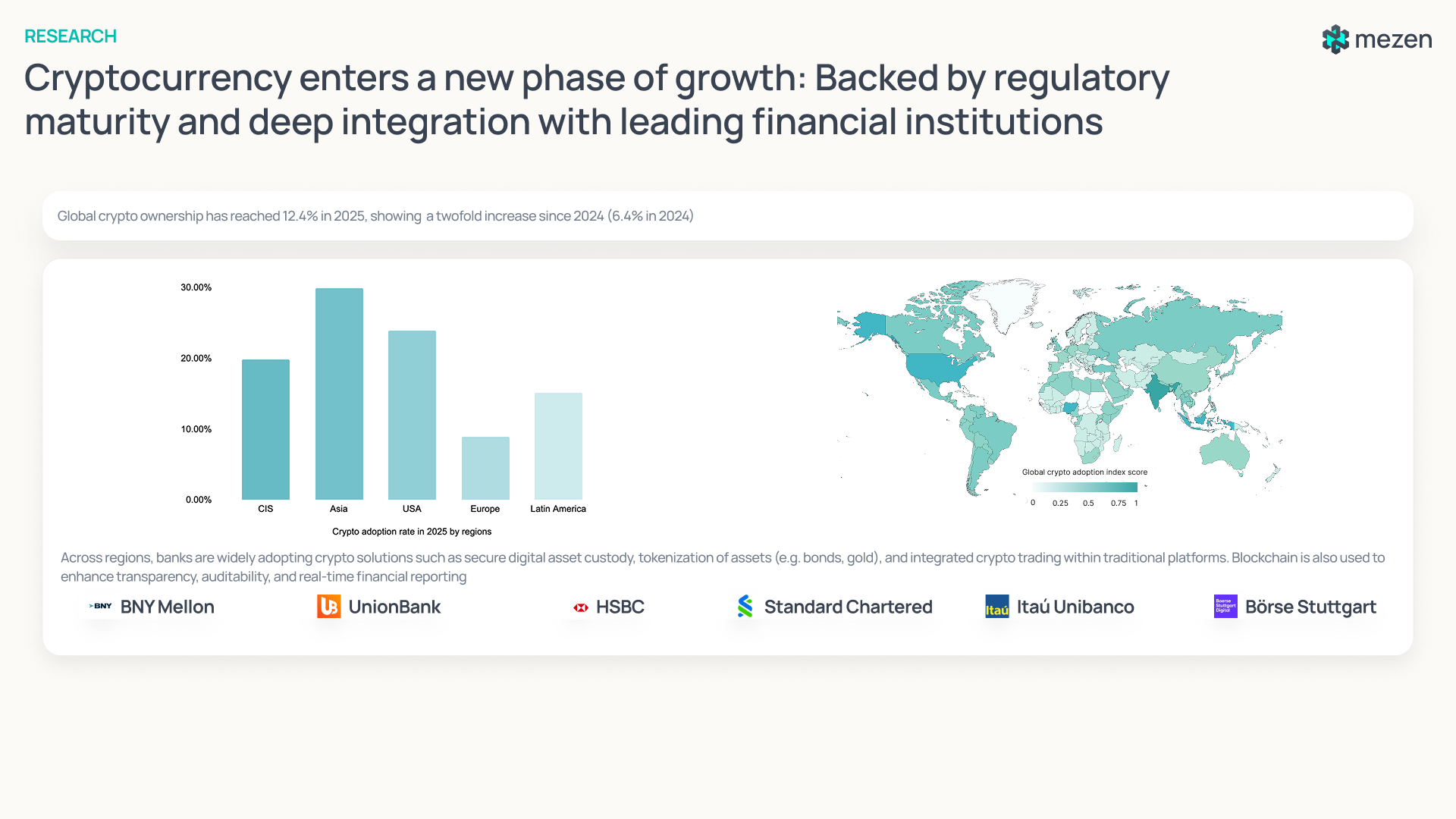

Crypto is steadily moving toward the mainstream. In 2025, global ownership reached 12.4% of the population — that’s around 700 million people.

- United States: 22–24% of the population

- United Kingdom: 24%

- France: 21%

- Vietnam: over 20%

- Nigeria: a staggering 47%

- Latin America: sharp rise to 15.2%

- Africa: fastest-growing region, up 19% year over year

For comparison: online banking adoption in the early 2000s took over a decade to hit similar numbers. Crypto did it in half the time.

For banks, these numbers leave no room for doubt. Crypto is no longer a niche — it’s becoming part of everyday financial life.

Regulation: From fear to frameworks

The “wild west” days of regulation are fading. The new trend: structured frameworks that allow innovation but demand compliance.

- United States: The GENIUS Act (July 2025) gave stablecoins an official green light, with strict rules on reserves, audits, and dual oversight (federal + state). At the same time, the government outright rejected CBDCs — betting on private-sector innovation instead.

- Asia: Japan, Singapore, and South Korea have fully fleshed-out rules for custody, tokenization, and stablecoins. Vietnam and Thailand are testing sandbox models and even tax breaks for crypto. Hong Kong wants to be a crypto hub, but with tough restrictions on who can issue and advertise stablecoins.

- Latin America: Here, regulation is driven by necessity. Inflation and weak currencies push people toward crypto, so governments are catching up. Brazil legalized crypto as payment, Argentina rolled out VASP licensing, and Peru approved sandbox pilots for Bitcoin trading.

The message is clear: regulators are no longer asking whether crypto belongs in the system. They’re figuring out how to make it work safely.

Why banks suddenly care

So why are banks — historically slow, conservative, and regulation-heavy — now racing into crypto?

Because they are facing deep, structural problems:

- Security: 79% of U.S. banks reported unauthorized access last year. Fraud cost them $485 billion in 2023.

- Legacy IT: About 75% of IT budgets are spent just keeping outdated systems alive, leaving little space for modernization.

- Profitability: Net interest margins are shrinking, deposit costs remain high, and new Basel III rules add billions in compliance costs.

Crypto infrastructure offers real solutions: stronger custody, cheaper settlement, and new revenue streams. What makes them even more appealing is that they often come without the massive IT investment traditional upgrades demand.

The leading use cases

Across regions, several applications dominate:

- Digital asset custody — secure storage with offline keys and multi-layer protection.

- Tokenization — moving bonds, funds, or commodities like gold on-chain for efficiency and transparency.

- Integrated trading — giving clients the ability to buy and sell crypto directly inside banking apps.

- On-chain data and reporting — using smart contracts to provide real-time reporting and audit trails.

These are no longer pilots. They are running at scale inside some of the world’s largest financial institutions.

Case studies around the globe

United States — BNY Mellon

The world’s largest custodian bank has been in the digital asset space since 2022, offering BTC and ETH custody. In 2025, it added Digital Asset Data Insights, a platform that streams fund data directly onto Ethereum. Investors now see live, verifiable information without intermediaries.

BNY Mellon is expanding its role, adding on-chain data services for institutional clients and reinforcing its position in digital markets.

Europe — HSBC, Standard Chartered, Börse Stuttgart

- HSBC: Offers custody for tokenized securities and is developing tokenized gold via its Orion platform.

- Standard Chartered: Began spot Bitcoin and Ether trading for institutions in July 2025, combined with custody.

- Börse Stuttgart Digital: A regulated infrastructure provider that now earns about 25% of its group revenue from digital services.

Latin America — Itaú Unibanco and Prosegur

- Itaú Unibanco (Brazil): Integrated BTC/ETH custody and trading into its Ion app. Within months, over $1 billion in assets were processed, with user adoption climbing sharply.

- Prosegur (Argentina): Built a high-security “crypto bunker” to store private keys offline under regulator approval — a regional first.

Asia-Pacific — UnionBank (Philippines)

UnionBank launched the PHX stablecoin in 2019, followed by crypto ATMs and custody services through its mobile app. Its focus: bringing affordable, transparent financial services to rural communities.

CIS — Alfa-Bank & Sberbank (Russia)

- Alfa-Bank: launched its A‑Token platform for issuing digital financial assets — tokenized bonds, gold, and stock-linked instruments — under a regulated framework in 2023. In 2025, it enabled a large issuance via a gold mining company Seligdar, with digital assets offered through A‑Token.

- Sberbank: Announced crypto custody services in 2025 and launched structured products linked to Bitcoin and FX rates.

Where this leaves us

The battle lines between banks and crypto are gone. What we see now is convergence.

Regulators are setting the rules. Banks are modernizing with blockchain. And users — hundreds of millions of them — are beginning to see crypto as a familiar part of their financial lives.

For Web3 founders, this changes everything. Institutional adoption doesn’t just validate crypto in the eyes of investors — it also expands access to a scale that was unthinkable just a few years ago. When a bank like Itaú integrates Bitcoin trading for 60 million clients, crypto distribution reaches levels no exchange could achieve on its own.

It also raises the bar. Compliance, security, and transparency are no longer optional; they’re the baseline for anyone who wants to compete in this environment. And while that raises the bar for projects, it also lays the foundation for a market that is stronger, more stable, and more integrated with global finance than ever before.

The future of crypto isn’t separate from the financial system — it’s becoming deeply interconnected with it.

.png)

.png)