.avif)

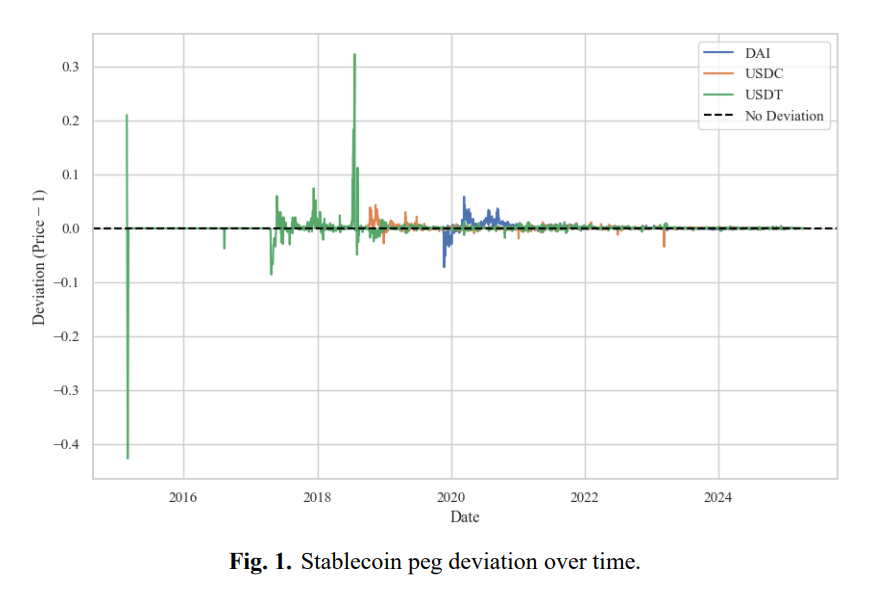

In October 2018, USDT, the largest stablecoin by volume, traded at approximately $0.87 on major exchanges. USDC, in its early period, regularly traded above $1. Neither outcome was a crisis. Both were normal for what the market was at the time: few participants, thin liquidity, slow arbitrage, fragmented trading across exchanges with no efficient way to close price gaps.

By 2019–2023, according to BIS data, stablecoins traded within a tight band of $1 approximately 94% of the time. Deviations became smaller. Recovery became faster.

The tokens themselves had not changed in any fundamental way. What changed was the infrastructure built around them, who could access redemption, how many participants were willing to arbitrage, and whether the market trusted that a $1 redemption was real.

That is the argument this piece makes: a stablecoin peg is a market outcome. And market outcomes are built.

Key Takeaways

- In October 2018, USDT fell to approximately $0.87. By 2019–2023, stablecoins traded near $1 around 94% of the time. The token didn't change. The market around it did.

- Peg stability comes from three layers: primary market access, secondary market arbitrage, and participant trust, and it requires all three simultaneously.

- USDC maintained an average secondary-market discount of ~1 basis point. USDT's was ~55. The gap traces to one variable: USDC had 500+ monthly arbitrageurs; USDT had roughly 6.

- Reserves don't hold the peg. They create the conditions under which the market can hold it if redemption access is fast, broad, and predictable.

- Trust is structural. It determines whether participants arbitrage or step aside. Tether's elimination of commercial paper in 2022 shifted that calculation without changing the token's design.

How the peg forms: three layers

Peg stability is the result of three layers working simultaneously. Remove any one and the other two cannot compensate.

- The first is the primary market, the direct channel between issuer and authorized participants for minting and redeeming at $1. It sets the economic anchor.

- The second is the secondary market: exchanges, DEXs, OTC desks, where the actual price forms and where arbitrageurs act on the primary market anchor to pull it back toward $1.

- The third is the trust layer, the set of beliefs participants hold about reserve quality, redemption speed, and issuer reliability. It determines whether participants choose to arbitrage at all.

None of these layers works in isolation. A well-designed primary market with no arbitrageurs produces deviations that persist. A deep secondary market built on fragile trust collapses the moment that trust does. The peg holds when all three are functioning at once.

Primary market as the anchor

The primary market is where the economic logic of a stablecoin begins. Authorized participants can mint or redeem tokens directly with the issuer at $1. If the market price falls below that, someone buys at a discount and redeems for a dollar. The spread is the profit. In theory, this alone should keep the peg tight.

What the theory skips is access. Primary market access is gated. Minimum transaction sizes, onboarding requirements, and settlement timelines that can run from hours to days mean that the theoretical arbitrage mechanism is only available to a limited group.

Federal Reserve Board research confirms the consequence: even with fully backed reserves, restricted or slow redemption directly reduces arbitrage efficiency. Deviations persist longer because fewer participants can act on them.

The primary market creates conditions under which the market can stabilize the peg. The distinction matters for issuers: a redemption mechanism that works on paper but is inaccessible at speed or scale is a design feature that the market cannot use.

Secondary market: where the peg actually holds

If the primary market sets the anchor, the secondary market is where the rope either holds or snaps. Price formation happens on exchanges and DEXs. When a stablecoin trades below $1, arbitrageurs buy it there and redeem with the issuer. The gap closes and the peg recovers.

How quickly that happens and how deep the deviation goes before it does depends on who is willing to act.

The USDT and USDC comparison from the 2021–2022 period makes this concrete. USDT averaged a secondary-market discount of around 55 basis points. USDC averaged approximately 1 basis point.

The difference in reserve quality or redemption mechanics between the two was not large enough to explain a 54-basis-point gap. The explanation sits elsewhere: USDT had roughly 6 active monthly arbitrageurs. USDC had more than 500.

More participants means smaller deviations, faster recovery, and less exposure to any single actor's willingness to trade on a given day. That is the structural finding and it points directly to what issuers need to build.

There is a second-order consequence worth naming. Research from the University of Chicago shows that more efficient arbitrage reduces deviations in normal market conditions but increases sensitivity to mass redemption events. Tighter arbitrage makes the system faster in both directions. Issuers should plan for that.

Breadth of listings compounds the participant depth dynamic. A stablecoin present across more venues and integrated into more use cases has more distributed liquidity. Localized imbalances, a spike in selling pressure on one exchange, get absorbed rather than amplified.

Trust layer: the variable that governs everything else

Reserve quality and transparency do not hold the peg mechanically. They determine whether market participants believe the peg is worth holding.

Tether's elimination of commercial paper from its reserves in 2022 illustrates this. The operational structure of the token did not change. What changed was the risk calculation for arbitrageurs and institutional participants who had been uncertain whether redemption would work as advertised under pressure. That shift in confidence had measurable market effects.

The BIS frames the underlying dynamic precisely: transparency's stabilizing effect is conditional on the starting level of trust. When trust is high, more disclosure stabilizes. When trust is fragile, the same disclosure can accelerate the reaction it was meant to prevent.

For issuers, this means the trust layer is a structural one. Participants will arbitrage only when they hold three beliefs at once: the redemption mechanism works, the token is genuinely worth $1, and the reserves can be liquidated fast enough to make that true under stress. All three must hold. A gap in any one is enough to produce hesitation and hesitation at the wrong moment is a depegging event.

What issuers must build

The USDT and USDC history produces a clear conclusion: peg stability is not designed in at launch. It is built over time through deliberate infrastructure decisions. Four of those decisions matter most.

- Distribute liquidity at the right market points. Liquidity needs to exist in DEX pools with direct arbitrage relevance: stablecoin/stablecoin pairs, direct USDC and USDT pairs and across CEX order books with key trading pairs. Incentive programs should be dynamic: liquidity rebates and market-maker programs need to intensify when deviations widen.

- Build institutional arbitrage at scale. Market makers, proprietary trading firms, and crypto-native funds with primary market access need to be onboarded with operational terms that go beyond access. KPIs should cover spread commitments, depth requirements, and minimum activity levels. The goal is to make arbitrage constant rather than episodic.

- Expand the participant base. The single biggest predictor of peg tightness is participant count. Concentration in a small number of institutional actors creates fragility, if those actors step back, there is no one to replace them. Reducing minimum thresholds, simplifying onboarding, and lowering barriers for smaller participants directly addresses this.

- Build stress-period protocols before they are needed. A system that monitors peg deviation, liquidity depth, and recovery speed with pre-defined responses at each threshold is not optional infrastructure. The time between a depegging event starting and confidence beginning to unwind is short. Issuers who have to design their response in real time will lose it.

Conclusion

The history of stablecoin pegs is a story about market infrastructure catching up to a promise.

USDT made that promise in 2014. The market took years to develop the depth, the participants, and the operational maturity to keep it reliably. USDC built tighter conditions around the same promise faster, which is why its peg deviation was 54 basis points smaller despite operating in the same market.

The lesson is direct: the peg you announce at launch is not the peg you will have. What you will have is determined by how many participants can arbitrage, how quickly they can access the primary market, and whether they trust that the dollar on the other side of the trade is real. None of those conditions are set at issuance. All of them are built.

Frequently Asked Questions

Why do stablecoin pegs break?

Stablecoin pegs break when arbitrage fails. That can happen because participants lack access to the primary market (mint/redeem), because liquidity on secondary markets is too thin to absorb selling pressure, or because trust in the issuer collapses and participants choose not to arbitrage even when the economics support it. All three layers need to function simultaneously. A failure in any one is enough to produce a depegging event.

What is the difference between the primary and secondary market for stablecoins?

The primary market is the direct channel between the issuer and authorized participants who can mint or redeem tokens at exactly $1. The secondary market is everywhere else: exchanges, DEXs, OTC desks, where price floats freely and must be pulled back toward $1 by arbitrageurs acting on the primary market anchor. The primary market sets the economic incentive. The secondary market determines whether enough participants can act on it fast enough to matter.

Why does USDC have a tighter peg than USDT?

Research from 2021–2022 shows USDC had more than 500 active arbitrageurs per month. USDT had roughly 6. That difference in participant depth explains most of the gap between USDC's ~1 basis point average secondary-market discount and USDT's ~55 basis points. More participants means faster correction and less dependence on any single actor's willingness to trade on a given day.

Do high-quality reserves guarantee stablecoin peg stability?

No. Reserves are a precondition. Even fully collateralized stablecoins depeg when redemption access is slow or restricted, when too few participants can act as arbitrageurs, or when market confidence in the issuer breaks down. Reserve quality affects trust, trust affects participation, and participation is what holds the peg. The chain has multiple links and needs all of them.

What should a stablecoin issuer prioritize to maintain peg stability?

Four things: broad liquidity distribution across CEXs and DEXs with dynamic incentive programs that respond to deviation; institutional arbitrage partners with defined KPIs covering spread, depth, and activity minimums; low barriers to entry for smaller arbitrageurs to prevent concentration risk; and a real-time monitoring system with pre-defined stress responses. Participant count is the strongest predictor of peg tightness, everything else serves that goal.

.png)

.png)