.avif)

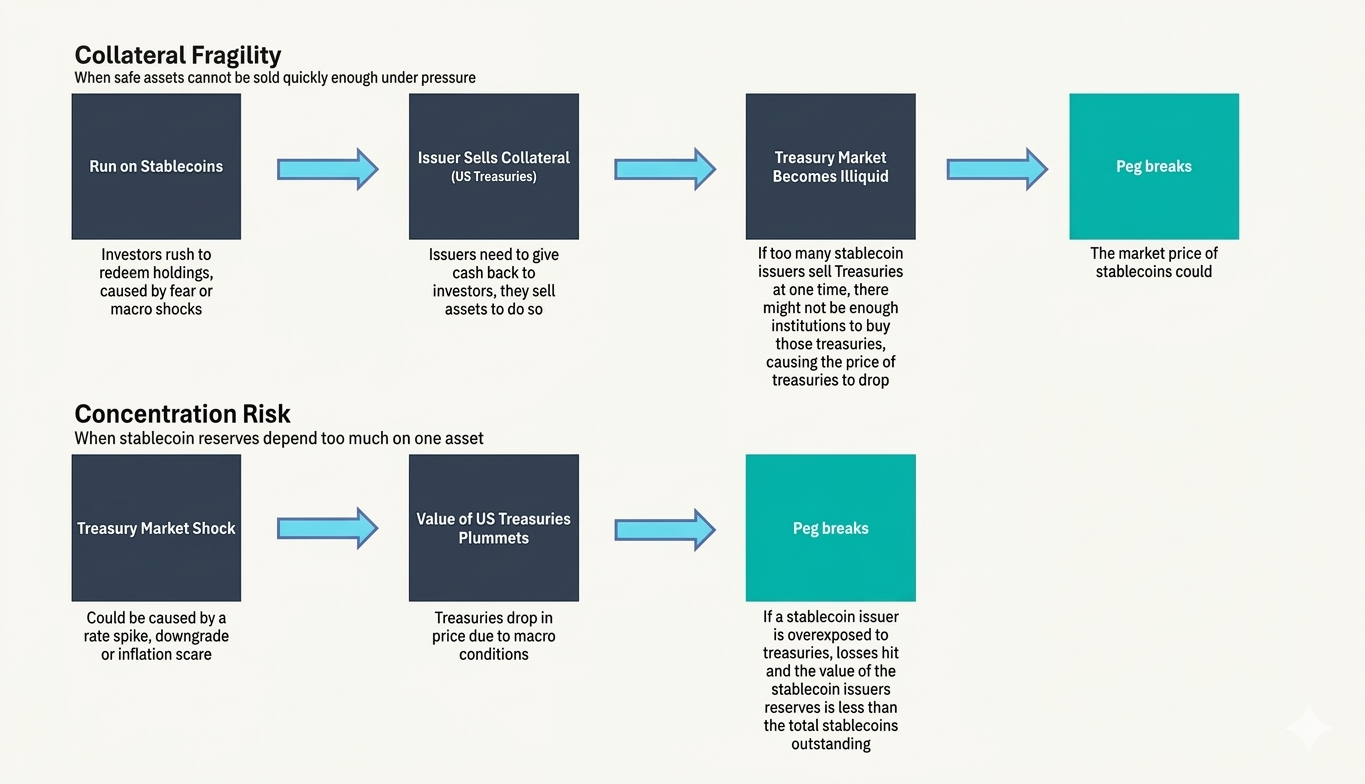

The USDC depeg of 2023 had nothing to do with bad reserves. The assets were fine, but they couldn't move fast enough. See why liquidity architecture matters more than what's in the vault.

Stablecoin stability is usually framed as a reserve quality problem. What assets back the token? Are they audited? Are they liquid? These are reasonable questions. They are also incomplete ones.

The deeper issue is speed. Stablecoins create obligations redeemable instantly at any hour, on any day, settled in seconds. The assets backing those obligations operate on a different schedule. Even the safest reserve instruments take time to convert to cash. When redemption demand outpaces available liquidity, the peg breaks, regardless of how sound the underlying assets are.

Key Takeaways

- Stablecoin stability depends on liquidity architecture. High-quality assets, including US Treasury bills, do not guarantee stability if they cannot be converted to cash faster than redemptions arrive. The USDC depeg in March 2023 was caused by $3.3 billion in reserves held at Silicon Valley Bank becoming temporarily inaccessible.

- The liquidity mismatch is structural. Stablecoins carry T+0 liabilities: instant redemption on demand. Most reserve assets settle at T+1 or slower. Depeg events occur when redemption volume exceeds immediately available liquidity.

- Concentration in T-bills creates systemic risk at scale. Tether and Circle together hold over $145 billion in US Treasury bills. In a mass-redemption scenario, forced selling could reach approximately 20% of average daily T-bill market volume. The BIS has documented stablecoin reserve flows already suppressing 3-month T-bill yields by 2.5 to 8 basis points depending on market conditions.

- Sound reserve management = balance sheet management. Dynamic rebalancing toward cash as stress indicators rise, diversification across custodians and instruments, and threshold-triggered liquidity policies separate robust reserve management from the alternative. Stablecoin issuers at scale are operating something functionally similar to narrow banks or money market funds and need to manage reserves accordingly.

Case 1: The USDC Depeg During the Silicon Valley Bank Collapse

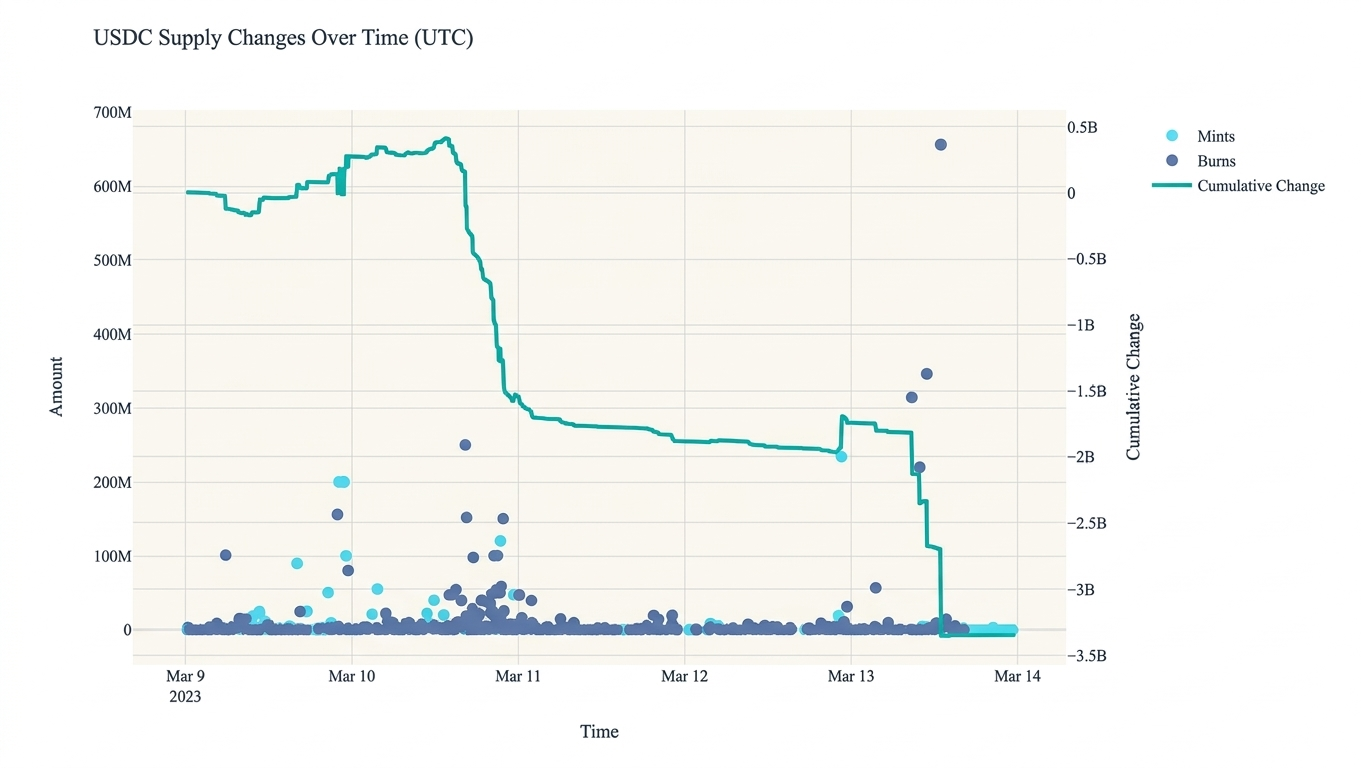

In March 2023, USD Coin, one of the largest dollar-backed stablecoins, temporarily lost its peg. Approximately $3.3 billion of Circle's reserves sat in Silicon Valley Bank when regulators shut it down.

Once Circle disclosed the exposure, three things happened in rapid sequence: USDC fell below $1 on secondary markets, mass redemptions began, and the broader market started questioning whether the reserves were actually accessible. The peg recovered fully once US regulators guaranteed all SVB depositors, but the recovery required government intervention.

The important distinction here is between reserve existence and reserve accessibility. The $3.3 billion was temporarily frozen and for a system built on instant redemption, temporarily frozen is functionally the same as gone.

This episode was one of the first times the market saw clearly: stablecoin stability depends on how fast those reserves can actually reach a holder requesting redemption.

Case 2: Stablecoins and the US Treasury Market

The second case is less dramatic, but more significant at scale.

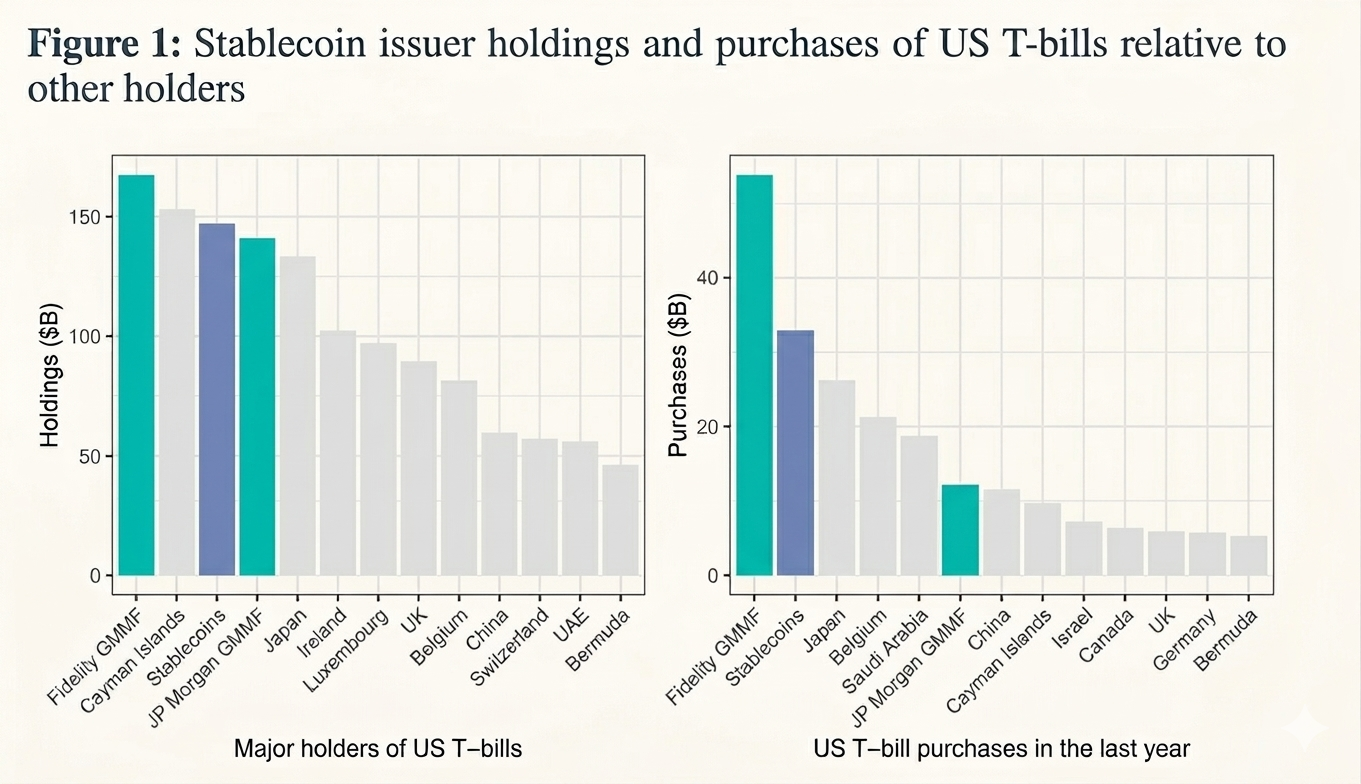

Tether and Circle, the two largest stablecoin issuers, invest a substantial portion of reserves in US Treasury bills. Together, their T-bill holdings exceed $145 billion. The logic is sound: short-duration sovereign debt is liquid, low-risk, and consistent with regulatory expectations taking shape in major markets.

The scale creates a new problem. In a stress scenario: mass redemptions across major stablecoins, issuers become forced sellers. Research estimates forced selling could reach approximately 20% of average daily T-bill trading volume. This is the fire-sale risk: rapid asset sales placing downward pressure on prices, creating losses for sellers and potentially spreading instability beyond the stablecoin market itself.

The BIS has documented the existing footprint. Sustained stablecoin inflows into T-bills suppress 3-month yields by roughly 2.5 to 3.5 basis points under normal conditions and up to 5 to 8 basis points during liquidity shortages. Stablecoin issuers are already large, permanent participants in the US government debt market.

The paradox is worth naming directly: the most reliable reserve assets can generate systemic risk when used to back obligations with instant redemption. High-quality collateral does not neutralize fire-sale risk. At sufficient scale, it creates it.

The Common Problem Both Cases Reveal

On the surface, these two cases look different. One involves inaccessible bank deposits, the other – potential forced selling of Treasury bills. The underlying architecture problem is identical.

Stablecoins create liabilities redeemable instantly and continuously: T+0. The assets backing those liabilities, even the safest ones, convert to liquidity more slowly and depend on the infrastructure of traditional financial markets: settlement windows, banking hours, counterparty availability. This gap between the speed of obligations and the speed of reserve liquidity is the structural mismatch at the core of every fiat-backed stablecoin.

As the stablecoin market grows, this mismatch stops being purely an internal issuer problem. It starts affecting traditional financial markets. With more than $145 billion in T-bill holdings, stablecoin issuers influence the pricing of one of the world's most important financial instruments. In a stress scenario, the liquidity problem at the issuer level becomes a volatility problem at the market level.

The reserve liquidity problem therefore operates on two levels simultaneously: for individual issuers, it is the risk of failing to meet instant redemptions; for the financial system, it is a potential source of pressure on sovereign debt markets when mass redemptions force rapid asset sales.

What Economic Models of Reserve Management Show

Academic models of stablecoin reserve management treat the issuer as a system permanently balancing two objectives: maximizing yield on reserves and maintaining sufficient instant liquidity for redemptions.

The key finding from these models: depeg events occur when redemption volume exceeds immediately available liquidity. A stablecoin can be fully solvent in aggregate and still fail to meet redemption demand in real time. Solvency and liquidity are different conditions, and only one of them matters in the moment a holder wants out. Three additional insights emerge consistently.

- Redemption flows cluster. One wave of redemptions raises the probability of the next, because each round signals potential instability to remaining holders. The self-reinforcing nature of redemption waves means the gap between a manageable outflow and a crisis can close faster than static reserve buffers anticipate.

- Average-day liquidity is the wrong target. Reserve management calibrated to typical daily flows will fail under the specific conditions most likely to produce a crisis. Optimal strategies need to be stress-tested against tail scenarios.

- Threshold policies outperform static allocations. The most effective reserve management approaches operate with trigger logic: during calm conditions, hold a higher share of yield-generating assets; when stress indicators cross a defined threshold, shift rapidly toward cash. The speed of rebalancing matters as much as its direction.

Practical Principles for Reserve Management

From the case analysis and economic modeling, five principles emerge for reserve management built around liquidity rather than quality alone.

Dynamic rebalancing

Reserve composition should not be static. During calm periods, a higher allocation to yield-bearing assets makes sense. When stress signals appear, rising redemption volumes, market volatility, counterparty risk indicators, the cash share needs to increase quickly. A reserve portfolio optimized for normal conditions and held unchanged through stress is a liability.

Threshold liquidity policy

The most effective approach is explicitly conditional: if stress signals remain low, portfolio structure stays unchanged; if risk crosses a defined level, liquidity increases sharply. This threshold logic prevents unnecessary yield sacrifice during calm periods while ensuring rapid response when it matters.

Diversification across instruments, custodians, and counterparties

The SVB episode illustrated custodian concentration risk directly. No single bank, T-bill maturity, or custody arrangement should represent a concentration severe enough to impair instant liquidity if it becomes unavailable. Diversification in this context is about eliminating single points of failure in the path from reserve asset to redeemed token.

Managing redemption flows directly

Some models propose using variable fees on token creation and redemption as a stabilization tool. These fees can slow redemption pressure during stress and buy time for orderly asset liquidation. The tradeoff is user experience; stablecoins built on frictionless redemption may resist fees as a design compromise, even when they serve a genuine risk management function.

Treating transparency as a two-edged instrument

This is the principle most often misunderstood. Reserve transparency builds confidence when market trust is already high, holders who can verify reserve quality feel less pressure to redeem preemptively. When confidence is fragile, the same disclosures can function as coordination signals. A holder reading a report showing concentration in a specific institution can update negatively and act, and doing so publicly may trigger others to follow. The disclosure meant to reassure becomes the focal point around which a redemption wave organizes. This is the paradox of transparency: its effect depends entirely on the level of trust and market expectations at the time of disclosure.

Non-USD Stablecoins and the Currency Dimension

One underappreciated aspect of the reserve liquidity problem is how it compounds for non-USD stablecoins.

Euro-denominated stablecoins remain a fraction of the overall market, the ECB places their circulation in the hundreds of millions. But the structural problem is worse for them. Euro-denominated reserve assets are less liquid in stress conditions, the secondary markets for euro-pegged tokens are thinner, and the regulatory frameworks are newer and less tested.

JD.com and Ant Group have reportedly lobbied for an offshore yuan stablecoin in Hong Kong, partly as a counter to growing dollar dominance in digital payments. If those projects proceed at scale, they will inherit the same liquidity mismatch between T+0 liabilities and slower-settling reserve assets but in a currency and regulatory environment with even less institutional infrastructure for managing it.

The dollar dominance of the stablecoin market is often framed as a geopolitical fact or a network effect story. It is also, partly, a liquidity fact: dollar-denominated reserves are more liquid, more widely traded, and more quickly convertible in stress than alternatives. For non-USD issuers building at scale, closing the gap on reserve liquidity is not optional.

The Regulatory Dimension in 2026

The GENIUS Act, signed into US law in July 2025, requires stablecoin reserves to be backed with liquid assets, US dollars, and short-term Treasuries, along with reserve disclosure requirements. MiCA in Europe establishes parallel authorization requirements for asset-referenced and e-money tokens.

Both frameworks represent meaningful progress, particularly in improving the quality and transparency of reserves. However, they stop short of addressing a more fundamental issue: liquidity mismatch.

As Anastasia Zenina, Strategic Consultant at Mezen, puts it, his mismatch is structural. Even high-quality, liquid assets can become a source of instability when they are held at scale against liabilities that can be redeemed instantly (T+0). In stress scenarios, this dynamic can trigger fire-sale risks, regardless of how safe the underlying assets are. Regulatory clarity on reserve composition is necessary, but it is not sufficient.

Recent signals from policymakers reinforce this concern. In March 2026, the European Central Bank (ECB) warned that the rapid growth of stablecoins could weaken monetary policy transmission and pull deposits away from traditional banks. This shifts the conversation toward a more systemic question: what happens when large-scale redemptions occur and how do those effects propagate through the financial system?

As stablecoins continue to grow, their reserves, often concentrated in instruments like Treasury bills, become increasingly intertwined with traditional financial markets. Large-scale redemptions would no longer be contained within the crypto ecosystem; they could exert direct pressure on core funding markets. The key risk is no longer just redemption itself, but how that stress spreads across the system.

From this perspective, tokenized deposits offer a structurally different approach. Rather than relying on external reserve assets, they represent traditional bank deposits on-chain. This eliminates the need to liquidate assets to meet redemptions.

Liquidity, in this model, already resides within the banking system, supported by central bank money and existing payment infrastructure. Instead of managing a mismatch, the model largely avoids it altogether.

This distinction becomes even more critical outside U.S. dollar markets, where liquidity is typically thinner and more fragile under stress. Over time, the competitive landscape may shift accordingly, not between individual stablecoins, but between two fundamentally different models:

- Asset-backed tokens, dependent on external reserves

- Bank-integrated tokens, embedded within the traditional financial system

The long-term outcome will likely depend on which model proves more resilient under real-world stress.

The Core Insight

Stablecoin stability is a liquidity problem. The assets can be excellent and the architecture can still fail, as happened to USDC in 2023 in a relatively mild scenario. At $300 billion in market cap and growing, the stakes for getting this right extend well beyond any individual issuer.

The projects and institutions approaching stablecoin reserve management with the seriousness it requires, building dynamic liquidity buffers, diversifying across custodians, stress-testing for correlated tail scenarios , are building systems with a plausible chance of surviving the conditions most likely to test them.

Everyone else is holding high-quality assets and hoping the gap between T+0 liabilities and T+1 settlement never becomes visible at the wrong moment. It will.

Frequently Asked Questions

What is the liquidity mismatch in stablecoin reserves?

The liquidity mismatch is the gap between the speed of stablecoin liabilities and the speed of reserve assets. Stablecoins promise instant redemption, T+0 settlement, at any hour. The assets backing those redemptions, even conservative ones like US Treasury bills, settle at T+1 or require active secondary markets to liquidate quickly. This mismatch is structural: it exists in every fiat-backed stablecoin design and cannot be removed without either slowing redemptions or holding only central bank reserves. The practical consequence is a stablecoin can be fully solvent on paper and still fail to meet redemption demand in real time if liquidity is concentrated in assets too slow to convert.

Why did USDC lose its peg in March 2023 if the reserves were legitimate?

Circle held approximately $3.3 billion of USDC reserves at Silicon Valley Bank when regulators shut the bank on March 10, 2023. The funds were frozen pending resolution proceedings. For a stablecoin requiring instant redemption, temporarily inaccessible reserves produce the same immediate effect as insufficient reserves: the issuer cannot honor redemptions at par, secondary market prices fall below $1, and a redemption wave follows. USDC recovered fully once US regulators guaranteed all depositors, but the episode showed reserve location and custodian risk matter as much as reserve quality.

How large is the stablecoin market's exposure to US Treasury bills, and why does it matter?

Tether and Circle together hold over $145 billion in US Treasury bills as of early 2026, making stablecoin issuers among the largest non-government buyers of short-duration US sovereign debt. Under normal conditions, BIS research shows stablecoin inflows into T-bills suppress 3-month yields by 2.5 to 3.5 basis points. During liquidity shortages, the effect reaches 5 to 8 basis points. In a stress scenario involving mass redemptions across major stablecoins, forced selling of T-bills could reach approximately 20% of average daily market volume, enough to move prices materially. The assets considered safest for reserves are also the assets whose forced sale creates the most systemic pressure.

What is the paradox of transparency in stablecoin reserve management?

Reserve transparency is generally positive for stablecoin stability when market confidence is high, holders who can verify reserve quality feel less pressure to redeem preemptively. The paradox arises when confidence is already fragile. In low-trust conditions, detailed real-time reserve disclosures can function as coordination signals: a holder reading a report showing concentration in a specific institution can update negatively and act. If enough holders do so simultaneously, the disclosure meant to prevent a run can accelerate one. This does not argue against transparency; opacity creates worse long-run risks, but it means transparency should be paired with robust liquidity architecture rather than treated as a substitute for it.

What reserve management practices reduce stablecoin run risk in practice?

Four practices emerge consistently from economic modeling and case analysis. First, dynamic rebalancing: reserve composition should shift toward cash as stress indicators rise. Second, custodian and instrument diversification: no single bank, T-bill maturity, or custody arrangement should represent a concentration severe enough to impair instant liquidity if it becomes unavailable. Third, stress-scenario calibration: reserve buffers should be sized for correlated tail scenarios, simultaneous redemption pressure, and market disruption. Fourth, treating reserve management as a liability-driven investment problem: stablecoin issuers at scale face the same structural challenges as narrow banks and money market funds and benefit from applying the same frameworks, including liquidity coverage ratios and formal stress testing.

.png)

.png)